Green Fundamentals: Have Venture Valuations Found a Floor?

Data-driven discussion of climate technology, finance, and policy

I provide data-driven climate tech market analysis. Follow along to stay up to date!

This post and the information presented are intended for informational purposes only. They reflect solely the personal opinions of the author in his individual capacity. They do not reflect the views or opinions of any current, past, or future employer, organization, or affiliate.

Venture flows have stabilized, but growth will be stubborn until IPOs accelerate and LPs realize exits

The climate venture market appears to have found its footing, with capital inflows settling into a new equilibrium. The sharp valuation corrections of the past two years have largely run their course, and while valuations haven’t returned to 2021 levels, they never collapsed to the lows of Clean Tech 1.0. Investors seem to have accepted that climate tech is here to stay. However, sustained growth in the space will depend on an eventual resurgence of IPO activity, which remains sluggish.

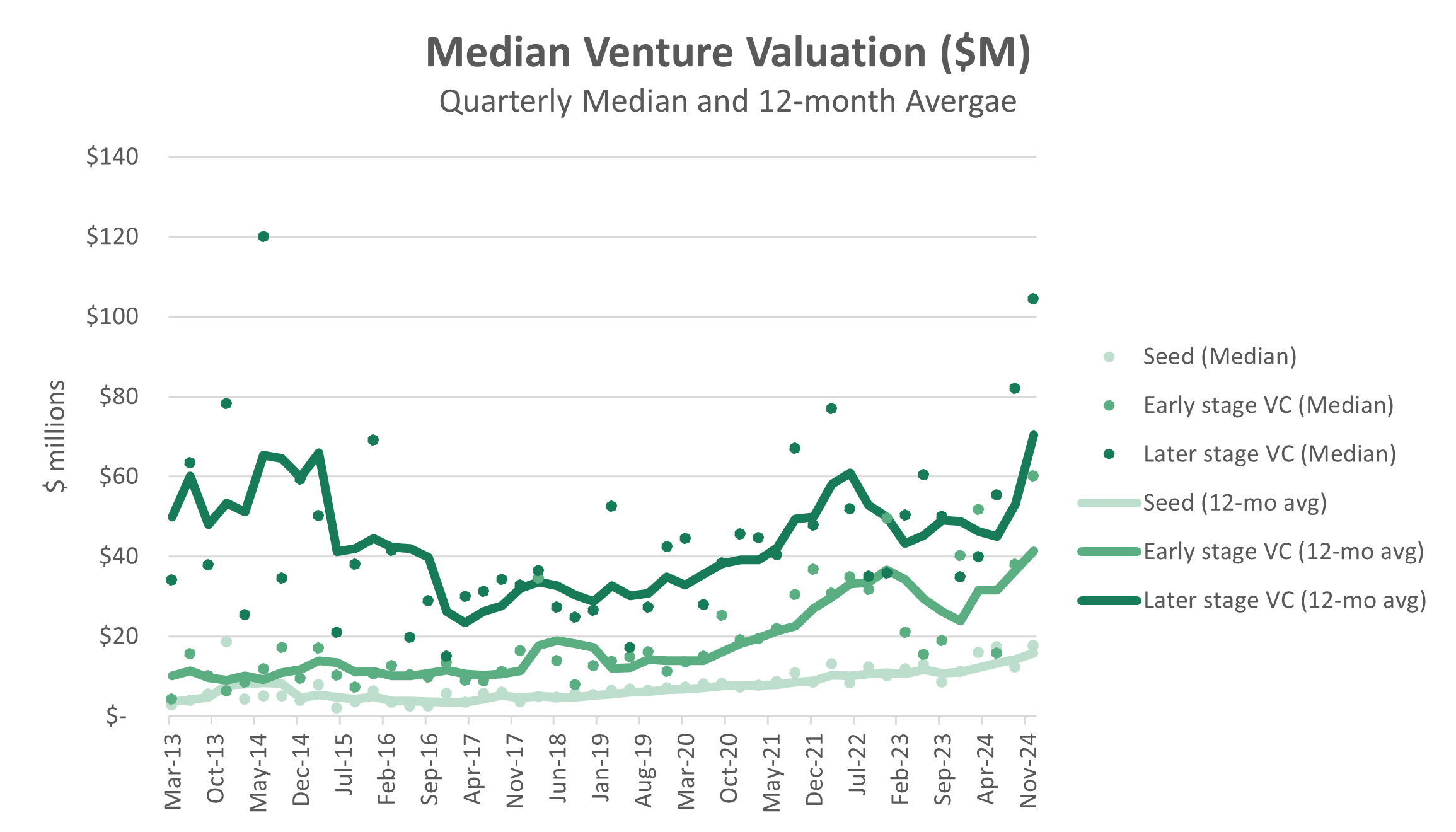

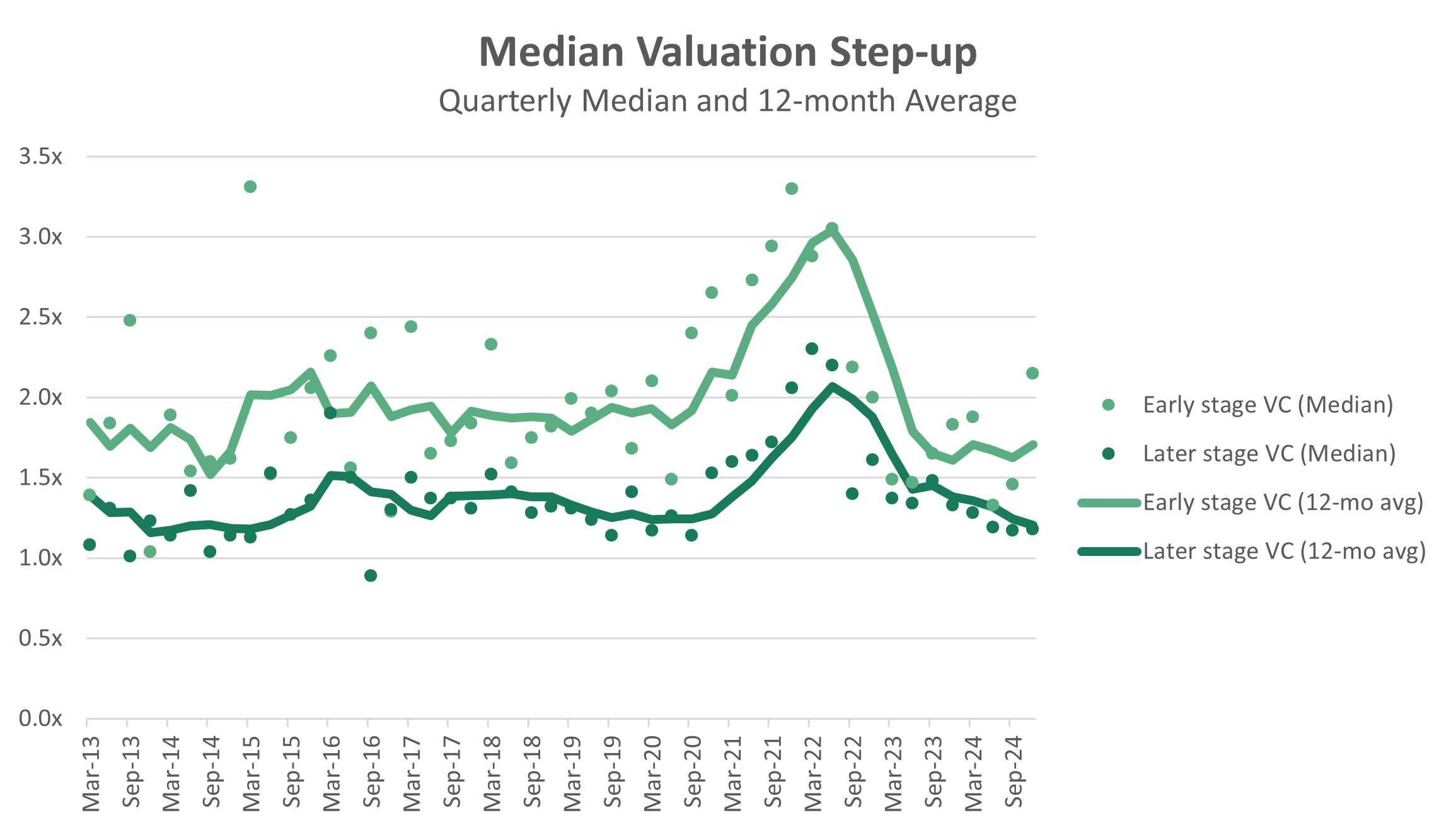

Valuations: The Bottom Has Passed—But Don’t Expect Skyrocketing Multiples

Over the past year, venture valuations stabilized and, in some cases, began to recover. Median pre-money valuations fell sharply in early-stage rounds, declining by 50.7% from 2023 to 2024, while growth-stage valuations continued their downward trend. However, valuation step-ups for early-stage deals appear to have bottomed out, signaling healthier capital conditions for startups looking to raise. The reset in valuations has brought step-ups back in line with pre-2021 norms, reinforcing the idea that climate venture is settling into a long-term sustainable trajectory.

Notably, late-stage pre-money valuations declined by 23.3% year-over-year, falling from $30 million in 2023 to $23 million in 2024. While early-stage valuations saw a sharper decline, this suggests that the capital market has been differentiating between proven and unproven business models, with more selective funding for later-stage ventures.

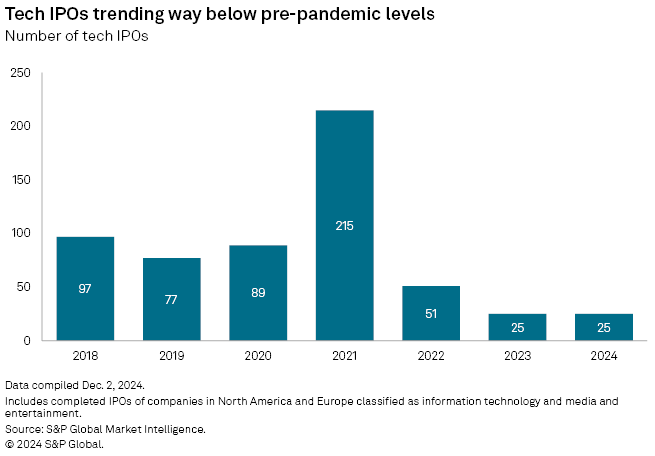

IPO Bottleneck Persists, But 2025 Could Be the Turning Point

The lack of IPOs remains a major constraint on venture growth. In 2024, only 42 VC-backed companies went public, the lowest level since 2011. This includes just 16 non-healthcare IPOs, a fraction of what was seen in previous cycles. Despite some high-profile public listings—such as Reddit, which surged to a $30 billion market cap from a $5 billion IPO valuation—the broader climate remains challenging. Investors remain cautious due to high valuation expectations and a demand for clear paths to profitability.

Looking ahead, S&P Global forecasts that IPO activity will return to pre-pandemic normalcy by late 2025, as inflation moderates and the Fed potentially cuts interest rates. However, a full recovery will depend on improved sentiment in public markets and macroeconomic clarity.

Source: S&P Global

Upcoming IPOs in 2025 include several climate-related companies poised to test investor appetite, including CoreWeave and Rivian (secondary offering). These will serve as key indicators of market confidence.

Source: U.S. News

In addition to these anticipated IPOs, CATL, the world's leading EV battery manufacturer, has filed for a secondary listing on the Hong Kong Stock Exchange, aiming to raise at least $5 billion. This move is intended to fund CATL's international expansion projects in Hungary, Spain, and Indonesia. Investors are closely monitoring this listing, focusing on how CATL plans to navigate geopolitical tensions, especially after its recent addition to a U.S. blacklist over alleged military ties—a claim the company disputes. The success of this offering could serve as a barometer for investor confidence in the EV supply chain amidst global economic uncertainties.

The Near-Term Outlook: Investors Should Expect Continued Uncertainty Until Mid-2025

Despite signs of stabilization, venture capital remains in a holding pattern. Investors and LPs alike are awaiting more clarity on economic data, federal fiscal policy, and bond markets before making aggressive moves. The resolution of key legislative uncertainties—such as the fate of the Trump Tax Bill and the U.S. federal budget—could provide further direction. If IPOs finally pick up, expect liquidity to flow back into the venture ecosystem. Until then, funding will remain available, but start-ups should not expect rapid valuation jumps.

See footnote for detailed valuation methodology and explanation.1

While technology companies are typically valued on Next Twelve Months (NTM) Revenue, traditional industrial businesses are often valued on Last Twelve Months (LTM) EBITDA. Due to the varied business models across climate tech (and the fact that many of the companies are not yet EBITDA positive) valuation multiples here are calculated based on Next Twelve Months (NTM) Gross Profit.

‘Climate Tech’ includes (1) any pure-play climate technology company that (2) has more than $200M market cap and (3) has positive revenue as well as gross profit (see sector deep dives for full list). ‘Traditional’ includes legacy market participants in relevant sectors (see sector deep dives for full list).

This post and the information presented are intended for informational purposes only. They reflect solely the personal opinions of the author in his individual capacity. They do not reflect the views or opinions of any current, past, or future employer, organization, or affiliate. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.