Green Fundamentals: Geothermal Tariff Boosts Clean Data Centers

Data-driven discussion of climate technology, finance, and policy

I provide data-driven climate tech market analysis. Follow along to stay up to date!

Google’s 24x7 Clean Energy Tariff sets the standard for data centers, utilities, and investors

What Happened: Google secured a groundbreaking new clean energy tariff from the Public Utilities Commission of Nevada (PUCN). The tariff enables Google to purchase 350k GWh of power (enough to power over thirty thousand homes for a year) from Fervo Energy’s geothermal plant through NV Energy. This initiative will significantly reduce Google's carbon footprint, eliminating approximately 140,000 metric tons of CO2 emissions annually.

Background: Data centers have struggled to procure 24x7 clean energy. This goal requires a constant supply of renewable energy, not just during peak production times like sunny or windy periods. Data centers are among the most energy-intensive operations, requiring constant and reliable power to ensure uptime and performance. Geothermal energy, which can provide consistent, base-load power, is a crucial part of this strategy.

Source: Goldman Sachs

Source: McKinsey & Company, Utility reporting

Fervo Energy recently announced the successful start-up of its first full scale commercial geothermal plant. Fervo utilizes advanced drilling and fiber-optic technology, traditionally used in the oil and gas industry, to create highly efficient and scalable geothermal systems that overcome traditional limitations related to resource location and depth. Fervo has secured ~100,000 acres of land likely suitable for their geothermal technology, including the 400 MW Cape Station project in Beaverton County, Utah (currently operational, PPA signed with Southern California Edison) and the 115 MW Corsac Station project in Nevada. Google had previously a 3.5 MW PPA in place with Fervo.

Source: Department of Energy

Existing procurement structures for renewable energy, including geothermal, face several limitations. Existing structures incentivize the production of the lowest cost power (like renewables when available) but do not accommodate or incentivize a premium for 24x7 output.

As a result, the new rate tariff structure made several innovations:

Fixed-Rate Pricing: The tariff involves a fixed-rate pricing model for the geothermal energy supplied by Fervo Energy. Unlike traditional variable pricing, which fluctuates based on market conditions and fuel costs, this fixed-rate model offers predictable and stable energy costs over the contract period.

24x7 Power Supply: The tariff ensures a continuous supply of geothermal energy, addressing Google's need for a reliable, around-the-clock power source. This is in contrast to traditional renewable sources like solar and wind, which are intermittent.

Energy Credits and Offsetting: Any surplus energy produced during periods of low demand is credited to Google’s account, effectively banking it for future use during higher demand periods. This ensures that any excess geothermal energy is not wasted and can be utilized when needed.

Regulatory Compliance and Reporting: The tariff includes stringent reporting and compliance measures to verify that the energy supplied meets Google’s carbon-free criteria. NV Energy and Fervo Energy must regularly report on energy production and usage.

Take-Away: The new Clean Energy Tariff allows the Nevada utility to sign a PPA for a technology they otherwise could not sign due to its relative cost. The right price signal from Google unlocks investment to bring more geothermal (and other clean, firm power) onto the grid. This contrasts with traditional renewable energy sources like solar and wind, which are intermittent and require storage solutions to manage supply during non-productive periods.

This newsletter has previously discussed how 24x7 clean power will command a premium. As data centers and industrial processes require more power, they are willing to pay a premium to low cost renewables to ensure they get clean power all day (and year) round. This bifurcation of the energy market is necessary to recognize the economic benefit of geothermal, long-duration energy storage, and nuclear.

What Comes Next: This agreement underscores the role of innovative tariffs and regulatory frameworks in facilitating corporate clean energy transitions. Other companies looking to decarbonize their operations around the clock might follow Google’s lead, exploring similar partnerships and technologies. Duke Energy announced in May an MOU with Amazon, Google, Microsoft, and Nucor for clean energy in the Carolinas.

The energy landscape is rapidly evolving, with new technologies and business models reshaping how companies approach their sustainability goals. As the cost and feasibility of different renewable energy sources improve, we can expect more groundbreaking agreements like Google’s. Investors and industry stakeholders who recognize the potential of these innovations will be well-positioned to capitalize on the shift toward a carbon-free future.

Further Reading

Technology (Deep Tech, Materials Science, Emissions)

Batteries: For EVs, Semi-Solid-State Batteries Offer a Step Forward (IEEE Spectrum)

Storage: Designer of World’s Tallest Building Wants to Turn Skyscrapers Into Batteries (Bloomberg)

Cement: Engineers Discovered the Spectacular Secret to Making 17x Stronger Cement (Popular Mechanics)

Water: California Water Temperatures Drop to Dangerous Levels (Newsweek)

Private Markets (PE / VC / Real Estate / Infra)

Wind: Legal Mess Ties Up $500 Million Wyoming Wind Farm Project (Cowboy State Daily)

Solar: The exponential growth of solar power will change the world (Economist)

Storage: Consumers Energy, Jupiter Power partner on Coldwater battery storage facility (Marketplace)

Storage: US sees 84% year-on-year rise in Q1 energy storage deployments, three states dominant (Energy Storage News)

Geothermal: Good news for 100% clean energy. Geothermal has finally arrived (LA Times)

Nuclear: Natrium Sodium Cooled Fast Reactor Starts Construction (Next Big Future)

Nuclear: Georgia Power customers paying extra after completion of state’s nuclear power plant (WSB-TV)

Utilities: How a new power plant near Modesto will help California avoid rolling outages this summer (The Modesto)

Uranium: Major Niger uranium mine back in public control (France 24)

Public Markets (Stocks, Bonds)

Solar: SolarEdge Technologies Stock Plunges on Customer Bankruptcy (Investopedia)

Electric Vehicles: Volkswagen's $5 bln investment in Rivian boosts EV maker's shares (Reuters)

EV Charging: EVgo and Regency Centers Open Newest Fast Charging Station in Longstanding Partnership, Expanding Footprint to More Than 120 Stalls Across U.S. (Business Wire)

Batteries: CATL, the little-known Chinese battery maker that has the US worried (The Guardian)

Utilities: PG&E Sees Power Demand Doubling by 2040 Thanks to AI and EVs (Bloomberg)

Utilities: California utility SCE seeks approval for 750MW of energy storage resource adequacy contracts (Energy Storage News)

Oil & Gas: Big Oil under pressure to recalibrate green transition goals (FT)

Oil & Gas: The giant Exxon project that could create the world’s last petrostate (FT)

Government & Policy

Metals: A New Geopolitical Melee Erupts Over Battery Metals (The Information)

Metals: US government stepping into battery metals where private capital is hesitant (S&P Global)

DOE: DOE doles out $900 million for next-gen small modular reactor deployment (Power Engineering)

Top 10 EV / NTM Gross Profit Multiples

See footnote for detailed valuation methodology and explanation.1

Top 10 and Bottom 10 Weekly Share Price Movement

Valuation Multiples over Time

As interest rates have increased, valuations of growth-focused climate tech have declined (similar to other growth-focused industries like cloud software), reducing the premium to their near-term focused, traditional industry peers.

The Top 5 Climate Tech companies account for all of the premium Climate Tech has over Traditional Industries.

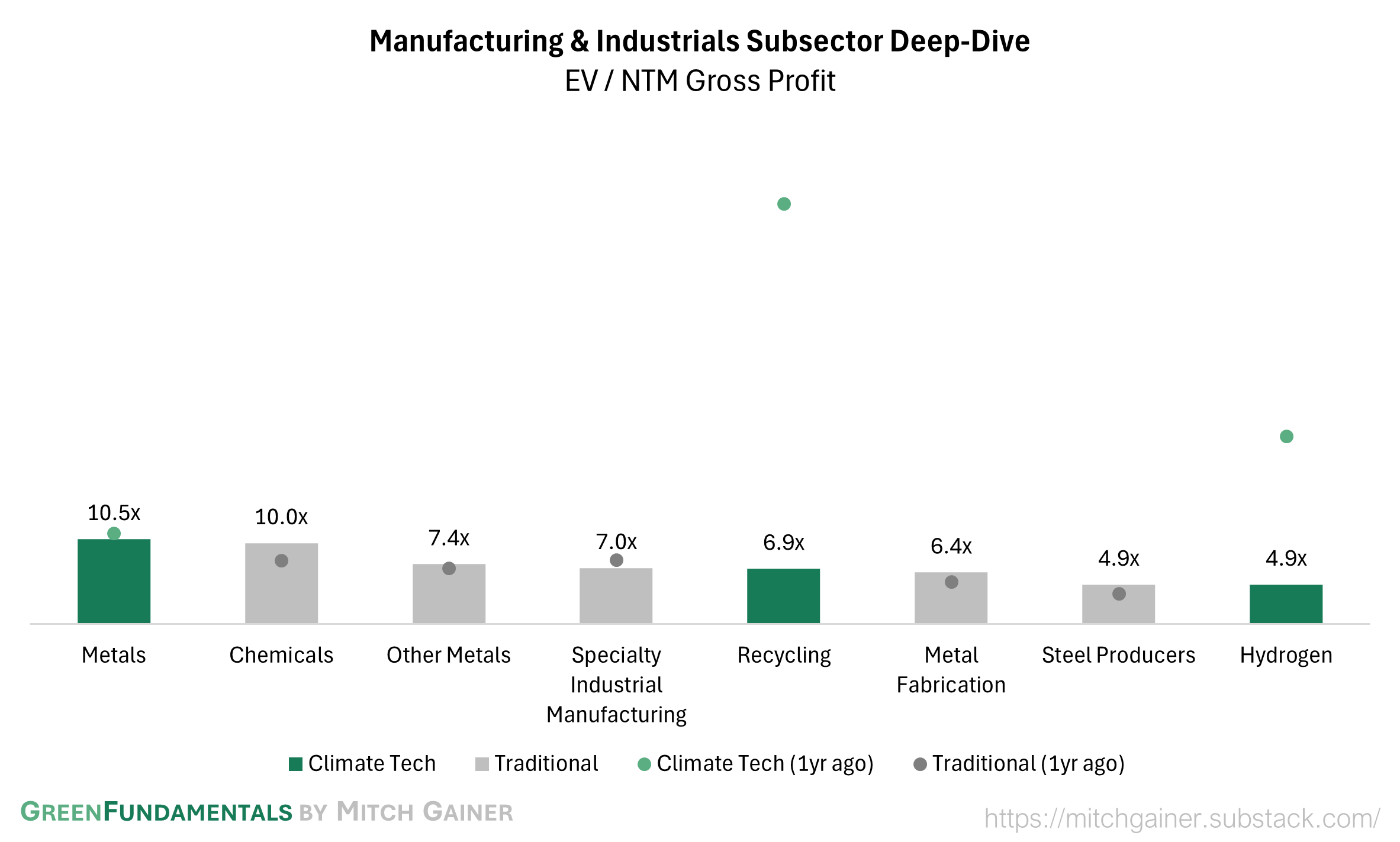

Deep-Dive by Subsector

Energy & Power: Mature and bankable climate tech (pure-play solar & wind, alt. power) commands a higher premium while energy management systems have increased in value; the market is more skeptical on hybrid solar & wind business models (combining manufacturing with services or operations).

Manufacturing & Industrials: Hydrogen is trading significantly lower because Ballard Power, which was previously excluded due to market cap, is now included in the comp set. As a result, the median for what is now a small qualifying hydrogen comp set moved significantly.

Transport: EV growth is priced in to climate tech and traditional companies - though they have declined over the past year; the market is skeptical on eVOTL.

Detailed Comparison Set Data

Sources include news articles cited (above) and publicly available SEC filings.

While technology companies are typically valued on Next Twelve Months (NTM) Revenue, traditional industrial businesses are often valued on Last Twelve Months (LTM) EBITDA. Due to the varied business models across climate tech (and the fact that many of the companies are not yet EBITDA positive) valuation multiples here are calculated based on Next Twelve Months (NTM) Gross Profit.

‘Climate Tech’ includes (1) any pure-play climate technology company that (2) has more than $200M market cap and (3) has positive revenue as well as gross profit (see sector deep dives for full list). ‘Traditional’ includes legacy market participants in relevant sectors (see sector deep dives for full list).

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.